Question

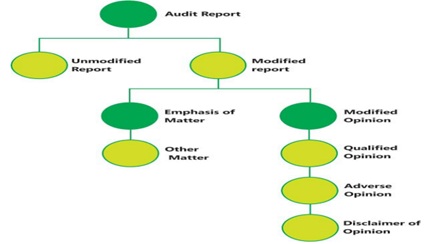

Which of the following is not a type of modified

opinion? Read the following passage and answer the next 4 question (Q23-Q26) The purpose of an audit is to enhance the degree of confidence of intended users of the financial statements. The aforesaid purpose is achieved by the expression of an independent reporting by the auditor as to whether the financial statements exhibit a true and fair view of the affairs of the entity. Thus, an audit report is an opinion drawn on the entity’s financial statements to make sure that the records are true and fair representation of the transactions they claim to represent. This involves considering whether the financial statements have been prepared in accordance with an acceptable financial reporting framework applicable to the entity under audit. It is also necessary to consider whether the financial statements comply with the relevant statutory requirements. The main users of audit report are shareholders, members and all other stakeholders of the company. SA 700 (Revised) - “Forming an Opinion and Reporting on Financial Statements”, deals with the auditor’s responsibility to form an opinion on the financial statements. It also deals with the form and content of the auditor’s report issued as a result of an audit of financial statementsSolution

The auditors’ opinion can be modified or unmodified. · Unmodified opinion – The opinion expressed by the auditor when the auditor concludes that the financial statements are prepared, in all material respects, in accordance with the applicable financial reporting framework. · Modified opinion – if the auditor concludes that based on the audit evidence obtained, that financial statements as a whole are not free from material misstatement or is unable to obtain sufficient appropriate audit evidence to conclude that financial statements as a whole are free from material misstatement. The modified opinion can be of various types – qualified opinion, adverse opinion or disclaimer of opinion.

Which of the following physical quantities is not conserved in inelastic collisions?

Which of the following signaling is involved in Paracrine signaling?

A ______ is a passive two-terminal electrical component that implements electrical resistance as a circuit element.

In the given figure, frogs occupy ________.

What is the minimum distance one has to stand at from a wall to hear an echo?

If a metal can be drawn into wires relatively easily it is called:

Which law explains why passengers move forward when a moving bus stops suddenly?

X-rays are

Which of the following is an example of a chemical change?

The primary function of bile in digestion is to: